The Case for Diversification: Protecting Wealth in an Uncertain World

By:

William Wang, CFP®, CEO & Financial Advisor

Megan Nichols, CFP®, Financial Advisor

Executive Summary:

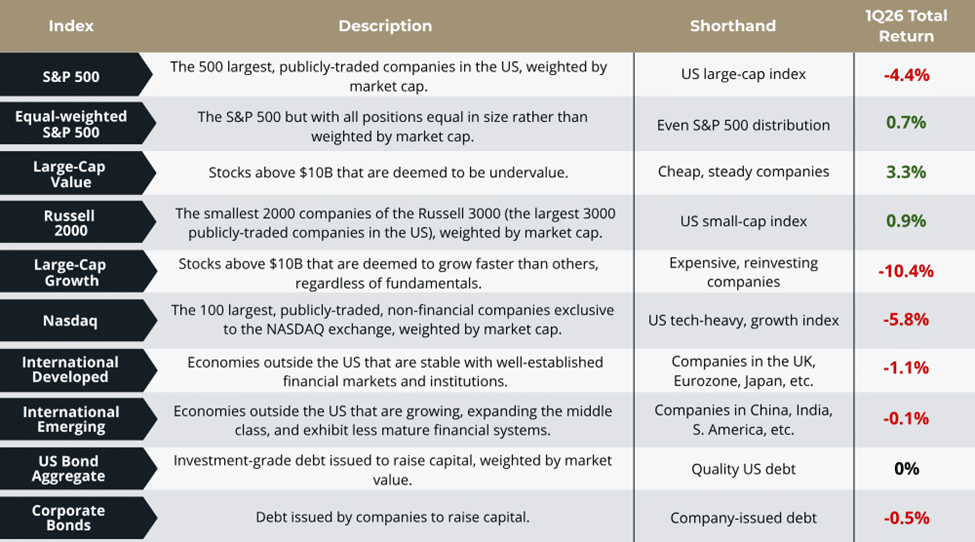

- The S&P 500 Index declined -4.4% in Q1, but the headline masked broad underlying strength. The equal-weighted S&P 500 gained +0.7%.

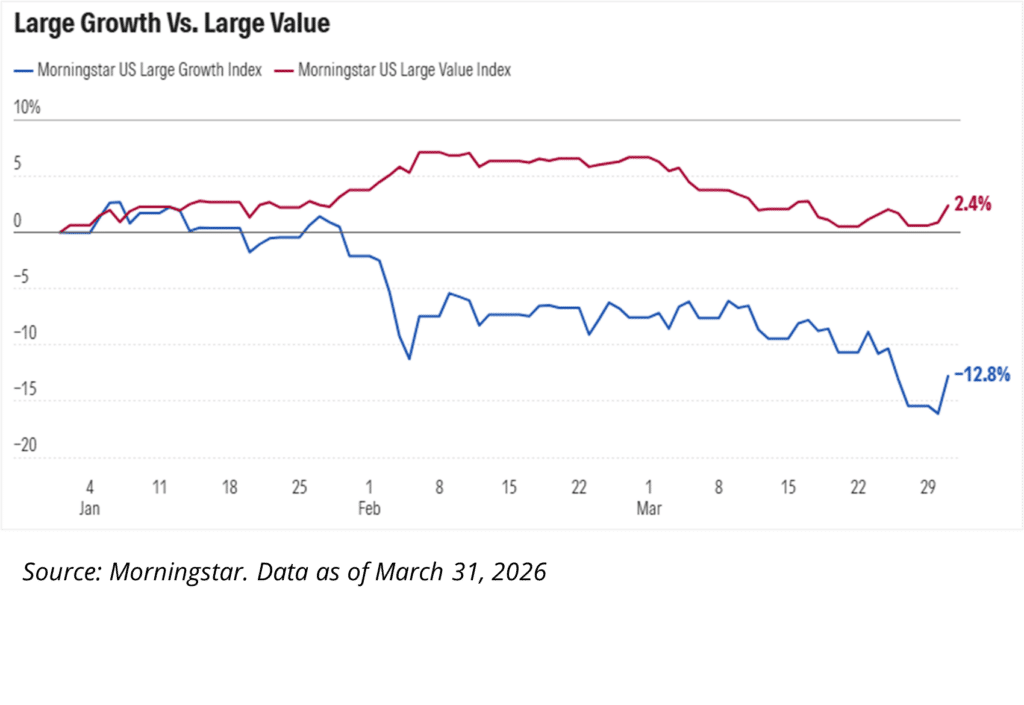

- Large-Cap Value rose +3.3%, and Small- and Mid-Cap added +0.9%, as the shift toward smaller and more value-oriented companies continued. In contrast, Large-Cap Growth declined -10.4% and the Nasdaq fell -5.8% as technology stocks came under pressure.

- International stocks outperformed the S&P 500 for a third consecutive month, with Developed Markets and Emerging Markets remaining flat.

- Bonds dropped in February only to increase just as rapidly in March with the 10-year treasury yield finishing at 4.32%.

In his 1994 letter to Berkshire Hathaway shareholders, Warren Buffett cautioned against the dangers of excessive risk and overconfidence, noting, “Only when the tide goes out do you discover who’s been swimming naked.”

As history has taught, it is impossible to accurately forecast the precise timing of economic downturns or geopolitical conflicts. Rather, the most prudent course of action is to construct a portfolio prepared for a variety of market environments.

In moments like these, before the tide recedes, the goal is to ensure that no single outcome can undo everything you’ve built.

This is why diversification remains a foundational risk-management strategy.

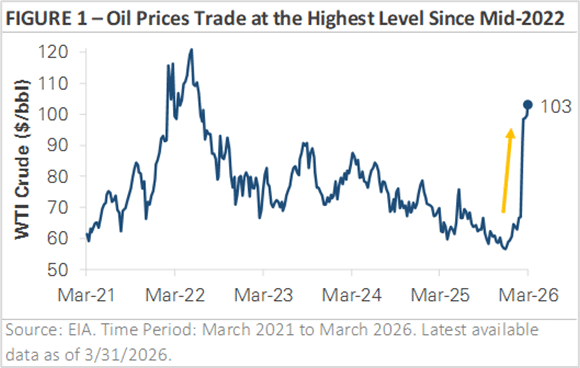

Market contractions have historically been a natural component of the financial cycle, frequently triggered by anticipated economic fear, sudden policy shifts and supply-chain disruptions that can rapidly alter market leadership. The current volatility in energy markets serves as a timely reminder that these shifts often arrive without warning.

As a result, prudent investors should exercise caution when investment strategies advocate for heavy concentration in emerging trends or encourage overexposure following a sector’s recent outperformance. Chasing market momentum frequently results in acquiring assets at peak valuations, thereby maximizing exposure precisely when the risk of a reversal is highest.

Ultimately, while diversification cannot guarantee positive returns, it remains the most reliable defense against market unpredictability. Sound wealth management is embodied by diligent preparation and prudent asset allocation, ensuring that portfolios are positioned to withstand the inevitable shifts in the economic tide.

The first quarter was eventful for markets.

Stocks traded higher to start the year, with the S&P 500 posting a modest gain in January. However, the market traded lower in March amid a spike in oil prices.

The S&P 500 returned -4.4%, but there were bright spots, despite the late-quarter volatility. The average S&P 500 stock outperformed the broad index by nearly +5% as market leadership broadened, and manufacturing data showed signs of improvement.

In January, crude oil gained nearly 13% as supply concerns related to Venezuelan output and Middle East tensions began to build. Prices increased another +4% in February, before sharply accelerating in March. The U.S.-Iran conflict and the closure of the Strait of Hormuz—a chokepoint for roughly 20% of global oil flows—sent crude oil prices surging nearly +50% in a single month. By quarter-end, oil prices had risen more than +70% overall.

Rising oil prices coupled with the risk of renewed inflation pressure led to a shift in rate cut expectations. At the start of 2026, investors anticipated two to three rate cuts by year-end. Those expectations, however, were steadily priced out over the course of the quarter, with the possibility of a rate hike being discussed as oil prices spiked in March.

Looking ahead, the situation remains fluid. Oil is trading near $100 per barrel, suggesting the market expects ongoing disruption, while developments in the Middle East will likely continue to influence short-term market direction.

The key development to watch in the coming months is the situation in the Middle East and its impact on oil prices. The Strait of Hormuz was still closed at quarter-end, with negotiations ongoing. Progress toward a resolution would likely ease energy costs and reduce inflation pressures, giving the Federal Reserve more flexibility on interest rate policy. A prolonged disruption would give higher oil prices more time to work their way through to the economy, potentially affecting consumer spending and business investment while keeping inflation elevated.

Ultimately, the relationship between oil prices, inflation, and Federal Reserve policy remains a key thread. Upcoming inflation data will be the first reports to capture the full impact of higher energy costs, and how those readings come in will shape the outlook for interest rates and the broader economy.

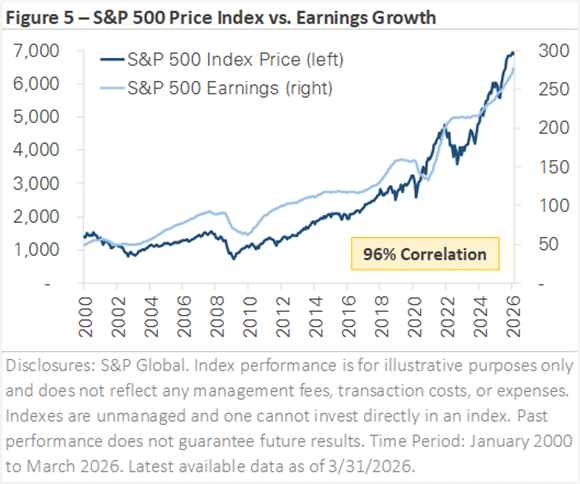

While the market’s decline in Q1 drew attention, it’s worth stepping back to look at the bigger picture. Figure 2 shows the relationship between the S&P 500’s price and its earnings over the past 26 years. The two have moved together with a 96% correlation. When earnings rise, stock prices generally follow. When earnings decline, as they did during the 2001 recession, the 2008 financial crisis, and the 2020 pandemic, stock prices tend to fall.

What stands out about the current environment is that earnings estimates have continued to rise even as the S&P 500 has pulled back. Profit margins remain healthy, and analysts still expect earnings growth in the coming quarters. The market’s decline has been driven by uncertainty around oil prices, inflation, and Fed policy, not by a deterioration in the fundamentals that drive stock prices over time.

That distinction is important for long-term investors.

Figure 1: Oil Prices Trade at Highest Level Since Mid-2022

Figure 2: S&P 500 Price Index vs. Earnings Growth

Heading into 2026, market sentiment resembled a delicate balancing act, with optimism about growth tempered by concern over inflation and rates potentially disrupting the balance. As the quarter unfolded, markets were reminded that economic transitions arerarely smooth. The quarter felt worse than it actually was, underscoring the importance of discipline, diversification, and long-term perspective during periods of uncertainty.

The economy can feel uncomfortable as it stabilizes because expectations often shift toward worry before the data shows signs of real deterioration, particularly during late-cycle transitions. Overall, the first quarter was a time of resetting those expectations. Heading into the second quarter, the picture is clearer, though challenges remain.

Most importantly, well-constructed portfolios and financial plans are made for periods like this.

Cooling, Not Collapsing

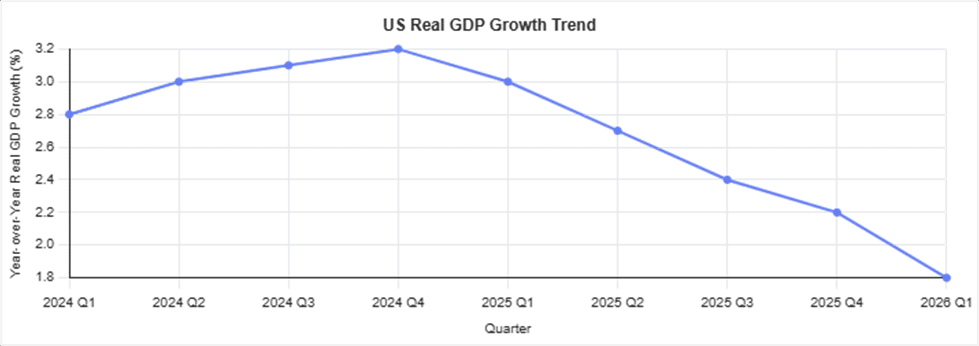

First quarter data for 2026 suggests the economy is slowing gradually, akin to a late-cycle slowdown rather than a sharp downturn. US growth is slowing from above-trend levels, the labor market is softer but still functional, and consumer spending remains supported, though uneven.

The Atlanta Fed’s GDPNow estimate for 1Q 2026 real GDP growth indicates a slowdown to roughly 1.6%–2.0%, down from above 3% in late 2025, reflecting softer consumer spending growth and slower inventory accumulation rather than widespread economic stress.

Payroll growth was well below prior-year levels but sufficient to keep the unemployment rate stable. In March, employers added 178,000 jobs, while the unemployment rate held near 4.3%, underscoring a labor market that is cooling but not contracting.

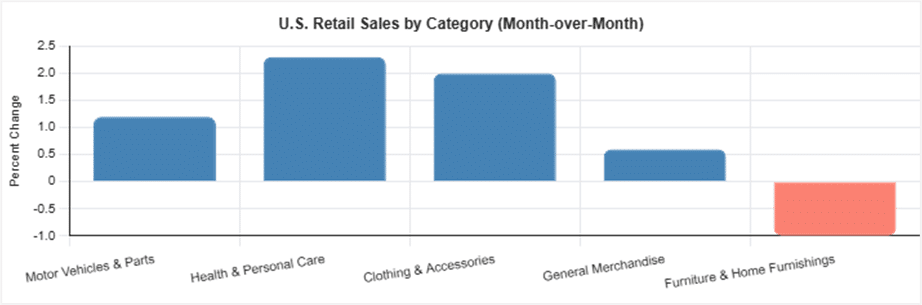

Retail sales rebounded late in the quarter, driven by motor vehicles, health‑related spending, and discretionary categories, as higher‑ticket items like furniture lagged. This pattern suggests elevated prices and borrowing costs are influencing where households are willing to spend.

Cooling demand, normalizing labor conditions, and reduced excesses often precede longer-term economic stability, though they can feel uncomfortable in real time.

US Census Bureau (Source: US Census Bureau (Advance Monthly Retail Trade Report, February 2026)

The Fed’s Narrow Path

Entering 2026, the Federal Reserve was facing a growing tension between its two, sometimes conflicting, mandates: 1) promoting a strong job market and 2) stable prices.

On one side, inflation had cooled meaningfully from earlier peaks, and price stability was improving, though not decisively achieved. Goods had largely normalized, but services (particularly housing-related costs, insurance, and healthcare) remained sticky.

On the other side, the labor market was no longer overheating as hiring had slowed, job openings had declined, and wage growth was moderating. However, unemployment remained low by historical standards, layoffs were limited, and firms were generally reluctant to shed workers. Neither mandate was flashing red, but both were drifting toward discomfort at the same time.

After reviewing first-quarter data, the Fed expects slower growth and a longer path back to their 2% inflation target, keeping rates elevated for now. Since investors entered the year expecting multiple rate decreases in 2026, expectations were adjusted and it was felt throughout markets.

Importantly, history suggests these environments often resolve not through abrupt policy moves, but through time and normalization. While rate cuts may come slowly and unevenly, higher-for-longer does not necessarily mean higher forever.

Your Portfolio Was Made for This

Equity markets posted solid gains in 2025, thanks to resilient economic growth, strong corporate profits, and continued artificial intelligence enthusiasm. The volatility markets experienced to start the year reflects a normal transitionary phase of the economic cycle.

Markets tend to adjust to changing economic conditions ahead of official data and headlines, and first-quarter performance reflected a recalibration of expectations rather than a reassessment of long‑term fundamentals.

By the time concerns dominated the news cycle, asset prices were already incorporating slower growth assumptions, more measured expectations for interest rate cuts, and greater differentiation across regions, sectors, and styles. This forward-looking nature explains why volatility increased without translating into broad market breakdowns.

Markets reallocated capital toward areas better aligned with the environment, favoring companies with durable earnings, pricing power, and balance sheet strength, while reassessing valuation and growth assumptions elsewhere.

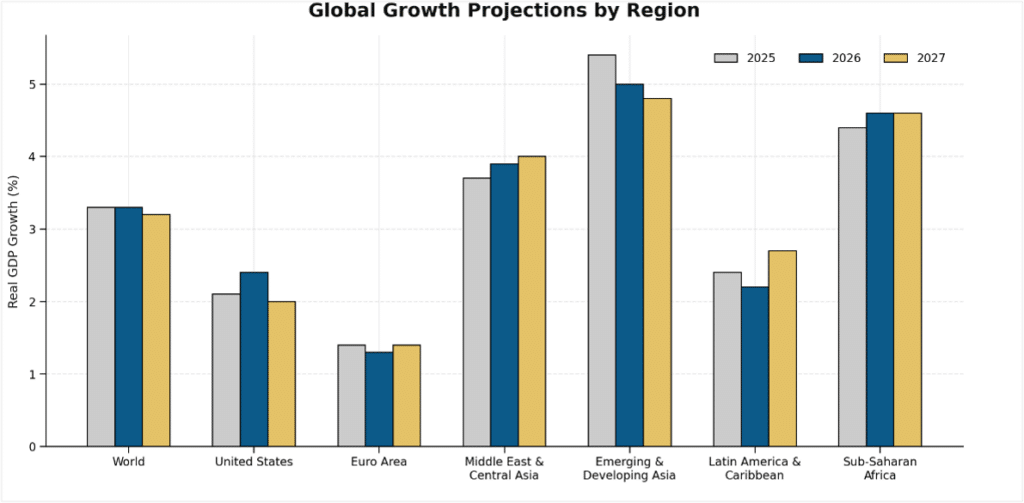

Global economic growth remains positive overall, but it is increasingly uneven across regions. The world economy is still expanding at a moderate pace, supported by technology investment, services demand, and fiscal support, particularly in the United States and parts of Asia.

In contrast, Europe continues to lag, constrained by higher energy costs, weaker manufacturing activity, and long‑standing structural challenges. Many emerging markets are growing faster on average, but outcomes vary widely depending on exposure to commodities, debt levels, and financial conditions. Geopolitical tensions, trade fragmentation, and energy price volatility have further amplified these differences, leading to a global environment where growth persists, but not uniformly, and with increasing dispersion across countries and regions.

Periods of transition tend to reward diversified portfolios built with both growth and income in mind. As markets adapt to a more uneven global backdrop, income-generating assets and diversification have re‑emerged as important contributors to resilience and long‑term results. A well‑designed financial plan recognizes market volatility as an inevitable part of the journey and is built to withstand a wide range of economic and market environments.

Remaining focused on long‑term objectives, supported by diversified portfolios and thoughtful financial planning, remains the most reliable way to navigate periods of uncertainty.

Source: IMF, World Economic Outlook Update (January 2026) | Notes: 2025 estimates, 2026-2027 projections. Prepared by HFG Trust for informational purposes only.

- Quarterly Market Review – Q2 2026

- Don’t Leave College Tax Credits on the Table

- SpaceX’s Public Market Debut: Opportunity, Expectations, and What Investors Should Consider

- Why Everyone Should Have a Power of Attorney

- Quarterly Market Review – Q1 2026