September 17, 2025

The Federal Reserve, known as the Fed, is the central bank of the United States, tasked with managing monetary policy to promote economic stability and growth. It sets the Federal Funds rate, influencing short-term interest rates.

The latest Federal Open Market Committee (FOMC) met on September 17, to discuss its dual mandate of promoting maximum employment and stable prices, and to discuss actions being taken to achieve both.

Interest Rates

The FOMC cut the federal funds rate 25 bps, bringing it to a range of 4.0% to 4.25%. The Fed is also continuing to reduce its securities holdings, a sign of quantitative tightening, to reduce money supply; this runs in opposition to the interest rate cut, as QT tends to increase interest rates. In other words, the Fed cut rates to aid the labor market but is engaging in QT to control inflation through reduction of the money supply.

…

Source: PIMCO, https://www.pimco.com/us/en/resources/education/everything-you-need-to-know-about-bonds, Accessed September 26, 2025

…

Inflation

The committee held firm in their long-term goal to maintain 2% inflation, while noting that core inflation currently sits at 2.9%, above earlier estimates. Near-term inflation estimates have risen, in part due to tariffs, with expectations for this year sitting at 3.0%. Inflation has predominantly been on goods while services are showing signs of easing. Looking ahead, the FOMC expects long-term inflation to decline to 2.6% next year and 2.1% by 2027.

..

Economic Growth

The FOMC noted that economic activity moderated in the first part of the year, averaging 1.5%, largely due to a decrease in consumer spending. This is down from 2.5% last year. Real GDP growth is now expected to be 1.6% this year, gradually rising to 1.8% in 2026 and 1.9% in 2027, slightly above previous estimates.

..

Labor Market

Employment growth has slowed, and the latest reports suggest the labor market is softer than previously anticipated, with lower

immigration contributing to the trend. While risks to employment have increased, the pace of job creation has fallen below the level needed to keep the unemployment rate steady. In response, the FOMC has taken action, and current projections show the unemployment rate rising modestly to 4.5% this year before gradually easing to 4.4% and 4.3% over the next two years.

..

Monetary Policy Outlook

Committee members remain divided on the path of the Fed Funds Rate, with varying views on whether additional cuts or a rate increase may be needed before year-end. With two meetings remaining, the Fed emphasized that future decisions will continue to be guided by incoming economic data. Current projections for the Fed Funds Rate are:

2025 – 3.6%

2026 – 3.4%

2027 – 3.1%

..

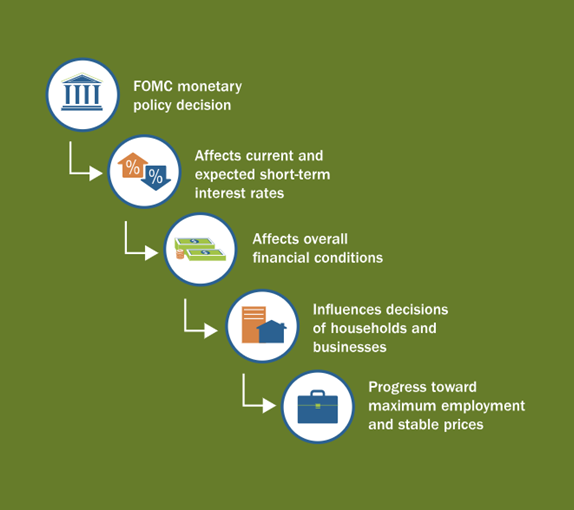

Source: The Federal Reserve Explained, https://www.federalreserve.gov/aboutthefed/fedexplained/monetary-policy.htm, Accessed September 26, 20256, 2025

..

Closing Thoughts

The politicization of the Fed dominated this meeting. It followed President Trump’s call for the removal of Lisa Cook and marked the first appearance of Stephen Miran, chair of the White House Council of Economic Advisers. These developments appear to have influenced the range of policy guidance and could contribute to deepening divisions in guidance throughout the year.

The President has expressed a preference for a weaker dollar—an outcome that could support recent U.S. advances in AI by making exports more competitive and attracting foreign capital. Tariffs tend to weaken the dollar, while AI remains a potential growth driver. In his debut, Miran is believed to be advocating for multiple rate cuts before year-end. As a result, Chairman Powell faced pointed questions about the political environment but emphasized the Fed’s continued commitment to data-driven neutrality and its independence as an institution. He also noted that the wide range of opinions reflects a period of historically unusual growth, where there is no risk-free policy path.

Powell acknowledged that inflation remains above earlier estimates but framed the new policy actions as a measured risk-management approach: slowing job growth now poses a greater risk to the economy than rising inflation, which he views as largely a one-time effect from tariffs. The Fed is navigating pressures from both sides—slower growth and labor market weakness argue for cuts, while persistent inflation argues for hikes. Attempting to appease both—cutting rates while continuing quantitative tightening— illustrates the delicate nature of current policy, and this tension is expected to continue as new data emerge.

Markets reflected this uncertainty, rallying early, selling off, and finishing the day flat. Still, history may provide perspective: in each of the 20 instances when the Fed cut rates within 2% of all-time highs, the S&P ended higher the following 12 months. Of course, this is no guarantee of results, but history does tend to rhyme.

Even so, cutting rates amid rising inflation, higher unemployment, and slowing growth highlight the importance of preparation. The most reliable defense remains disciplined diversification and regular re-evaluation of goals across all time horizons and potential economic futures.

..